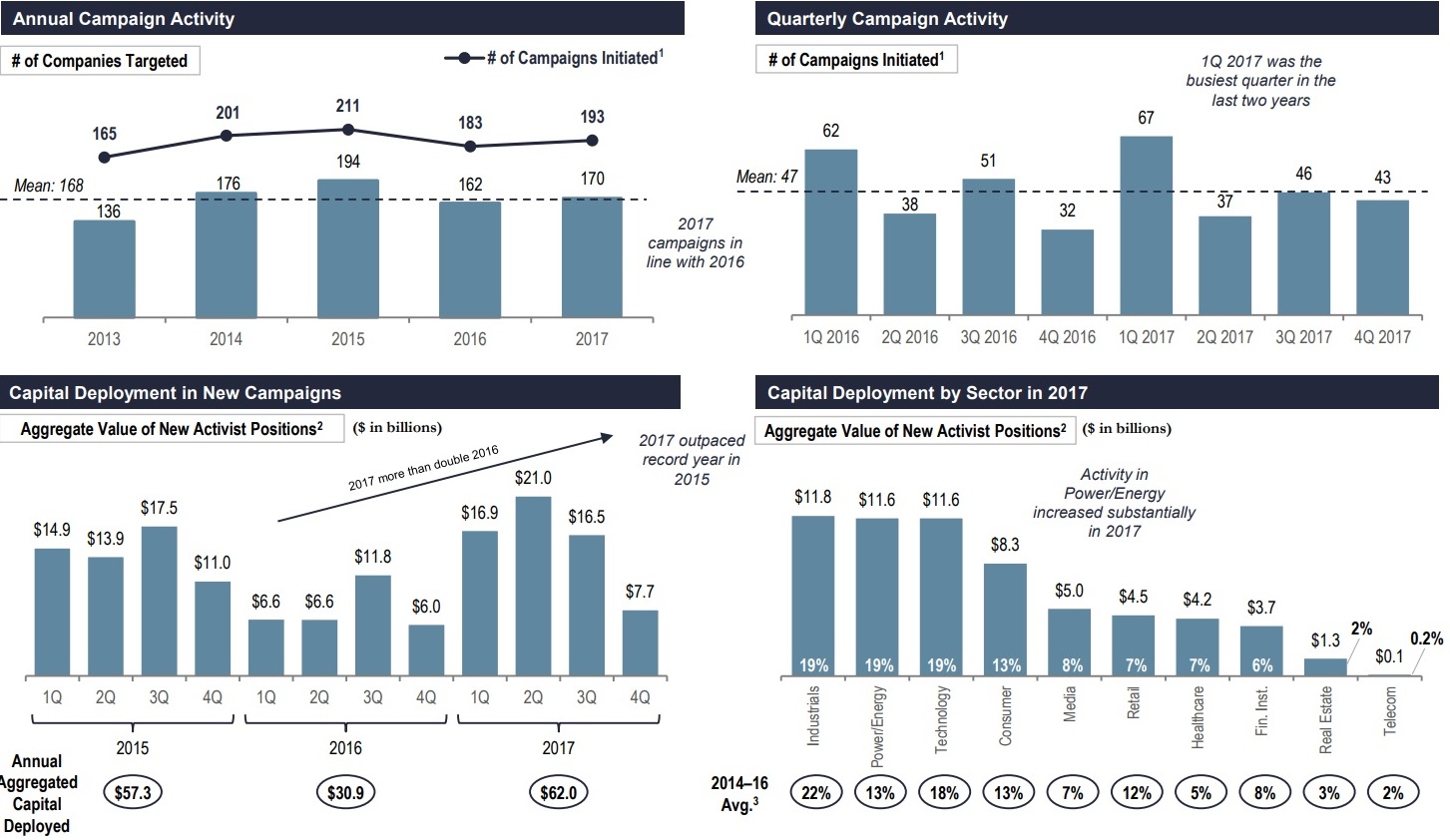

Activists deployed a record amount of capital in 2017, leveraging their credibility with traditional shareholders and access to large pools of capital to attack the largest companies globally

- Activists deployed a record amount of capital in 2017, leveraging their credibility with traditional shareholders and access to large pools of capital to attack the largest companies globally

- $62 billion deployed by 108 activists across 193 campaigns globally in 2017, more than double the total capital deployed in 2016

- Attacks on ADP, AkzoNobel, BHP, Credit Suisse, GM, Honeywell, Nestlé, NXP and Procter & Gamble confirmed that national champions and industry icons can be targets and that no company is immune

- Activists won an additional 100 Board seats in 2017, raising their five-year total to 551

- Campaign activity surged in Europe, driven by prominent U.S. activists turning abroad to find comparatively attractive valuation entry points and potential “low hanging fruit” for operational and strategic actions to enhance shareholder value

- Capital deployed in Europe increased to $22 billion in 2017, more than double the average of $10 billion deployed over 2013–16

- Nearly 30% of campaigns in 2017—a 65% increase compared to 2013–16—were against European targets, with U.S. activists—primarily Elliott, Third Point and White Tale (Corvex & 40 North)—accounting for over half of the activist capital deployed in Europe for the year

- High-profile proxy fights highlighted the increased independence and changing temperaments of large institutional investors, especially index funds

- The expanding influence of BlackRock, State Street and Vanguard continued to be felt across the governance landscape, from public statements by the firms’ CEOs on investment stewardship principles to more aggressive stances taken on gender diversity and climate risk

- Index funds showed an increased willingness to support dissidents in complex and consequential proxy contests (e.g., BlackRock supporting Pershing Square at ADP and Trian at P&G; State Street also supporting Trian at P&G and Land & Buildings at Taubman)

- The nexus between activism and M&A grew stronger, with the attractiveness of event-driven returns encouraging activists to assert themselves as a key player on the M&A chessboard and raising the appetite of strategic acquirers to adopt activism as a tactic

- Activist agitation led to numerous strategic and sale processes as the “fix” for underperforming businesses, and acquirers leveraged the disruption created by activism (e.g., Buffalo Wild Wings, BroadSoft, Parexel, SeaWorld, Whole Foods)

- Shareholder pressure resulted in the scuttling or sweetening of M&A deals that were poorly received by investors (SandRidge/Bonanza, Huntsman/Clariant, Qualcomm/NXP, Bain-Cinven/STADA, Safran/Zodiac, KKR/Hitachi Kokusai, GE/Arcam)

- PPG’s ultimately unsuccessful bid for AkzoNobel was assisted with pressure from Elliott, while Broadcom is running a slate of candidates to replace Qualcomm’s Board in an effort to complete its unsolicited bid for the company

Source: Lazard, Activist Insight, Fact Set, various public filings

____________

Why we Chart the Course? Charts speak a thousand words. They visually and concisely show economic, financial, and market trends. Charts help us build assumptions and conduct analyses for strategic decisions like exiting businesses, deploying capital, building investment portfolios, etc. In Charting The Course, we bring to your attention some of the charts we gather and analyze in our daily research and analyses of economy, business environment, investment and capital markets. We hope you find it of value.

_____________